Since part 4 of this series, a lot has changed with the US FinTech landscape that enables companies like Gusto to move money safely and speedily. In this part, we will look at some recent developments announced by NACHA, specifically around Same Day ACH.

Before we get going, make sure to refresh your memory on ACH basics and lingo from part 1, as well as on ACH timing from part 3.

So what’s new?

Same day ACH is a set of rules which give the option to ODFIs to transact money (debits or credits) and mandate RDFIs to settle funds on the same banking day. This theoretically allows Originators and Receivers to be able to send and receive funds within the same day.

In September 2016, Phase 1 of NACHA’s Same Day ACH rules became effective, allowing same day credits.

In September 2017, Phase 2 was rolled out for debits.

These enhancements come with some caveats, so let’s see if same day ACH is right for you.

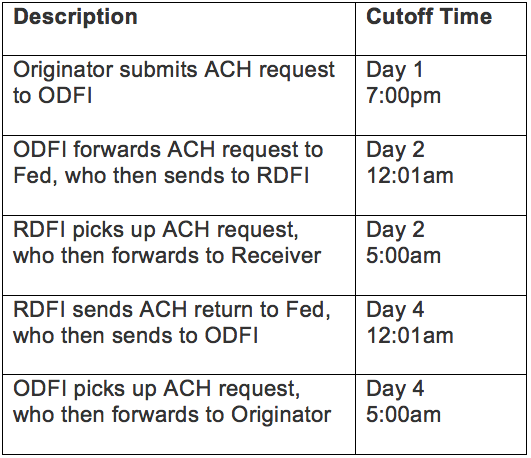

Regular ACH timing (all times in PT):

Same Day ACH timing:

Leg 2 and Leg 3 can now happen sooner on Day 1. There are 2 new windows for the ODFI to forward the ACH request to the Fed (and the RDFI) and for the RDFI to settle the funds.

Window 1: Fed receives ACH request by 7.30am PT, RDFI settles funds by 10am PT

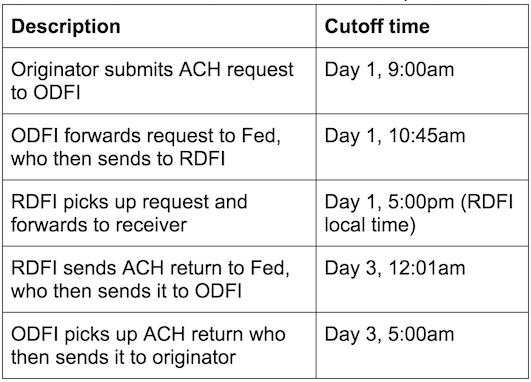

Window 2: Fed receives ACH request by 11:45am PT, funds settled by 2pm PT

In addition, with Phase 3 in March 2018, the rules mandate RDFIs to make funds available to Receivers by 5pm RDFI’s local time.

Here’s what the same day ACH timeline looks like for Window 2 (all times in PT)

How do I use it?

Originators can request same day ACH for transactions by setting the Effective Entry Date and Company Descriptive Date (check if required by your ODFI) fields to the same banking day as the day of submitting the the ACH file. These fields are on the batch header record of the ACH file.

Unfortunately, there are some practical limitations to be aware of before implementing same day ACH:

- International transactions (IATs) are excluded from same day ACH rules.

- ODFIs must set an earlier cut-off time to receive and process ACH files with same day entries from the Originator. In our case, the cut-off time set by our bank is 9am PT for Window 2. This in turn means that we would need an even earlier payroll run deadline to meet the final same day ACH window.

- There is a $25,000 per-transaction limit on same day ACH entries. NACHA guidance prohibits splitting larger transactions to work around this limit, but allows genuine use cases of multiple transactions between the same accounts on the same day.

- Banks are positioning same day ACH as an alternative to wires and pricing it accordingly. Depending on your relationship and contract with your bank, the per transaction cost can be more than 100 times that of regular ACH.

- Lastly but quite significantly - the timeline for leg 4 and leg 5 remains unchanged. This means RDFIs still have 24 hours to respond to the ACH request and it can still take 2 business days for the Originator to be notified of any returns. The “no news is good news” policy remains intact and even with same day settlement, it makes sense to wait at least 2 business days before you can assume that your transaction was successful.